If you’re looking to build steady passive income in Nepal, rental real estate remains one of the most reliable avenues. Not only can property deliver monthly cash flow, but it can also provide capital appreciation and inflation protection.

However, investing successfully requires local market knowledge, legal clarity, and careful financial planning. In this guide, you’ll find practical steps, data, and links to official sources so you can buy rental property in Nepal with confidence.

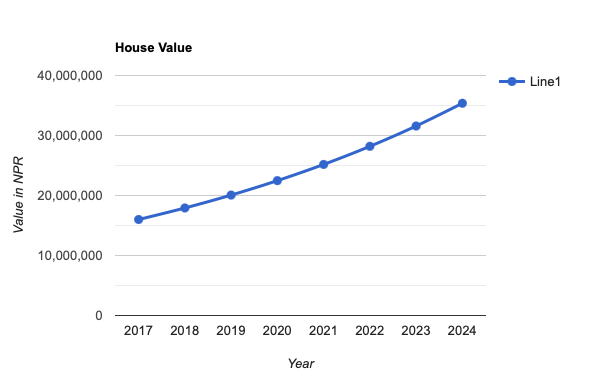

Why Invest in Rental Property in Nepal: Market Snapshot

First, some context. Major Nepali cities; Kathmandu, Lalitpur, Pokhara, Biratnagar, Birgunj and Chitwan have rising housing demand due to urban migration, tourism, and commercial expansion.

Gross rental yields in Nepal’s urban districts commonly range between 4–7% depending on location and property type, with tourist pockets or premium central areas sometimes higher. For example, localized analyses show Kathmandu yields near 5–7% for well-located apartments, while high-traffic tourist neighborhoods (e.g., Thamel) can see higher short-term income from serviced rentals.

Moreover, the real estate sector remains significant for bank lending and household wealth: Nepal Rastra Bank reports stable real estate lending volumes, and mortgage rates have been trending lower in recent quarters — mortgage interest rates in Nepal averaged around 8–11% in 2024–25 (check current NRB data before planning). Lower financing costs improve leverage returns for buyers using home loans.

Legal Framework: Who can Buy Property in Nepal?

Primary Laws, Rules and Regulations

1. Lands Act (1964) — Act No. 25 of 2021 (consolidated / amended)

Governs ownership, transfer, registration, land use ceilings, and registration procedures (Malpot). It is the principal statute that defines who may hold land and under what restrictions. Many of the rules that limit foreign ownership derive from this Act and its rules.

2. Lands (Land Rules) and Amendments

The rules under the Lands Act provide procedural detail (registration, transfer, excise, sample forms) and have been amended several times. Check the consolidated Land Rules for local procedural requirements.

3. Foreign Investment and Technology Transfer Act (FITTA), 2019 (2075) and FITT Rules (2021/2077)

FITTA is the primary legal framework for foreign investment in Nepal. It sets out how foreign investors may invest, the approval authorities (DOI, IBN), and the conditions for repatriation of funds.

FITTA does not automatically grant the right to hold land, but it describes when and how a foreign-owned company (or approved project) may acquire immovable property necessary for its operations by approval.

4. Companies Act / Business laws

For foreign investors the Companies Act (and related registration rules) governs how to incorporate a Nepali company (private limited, branch, or liaison), and such locally registered entities may acquire property if permitted under their approval and FITTA. The company route is frequently used for commercial land acquisition. MedhaCorpLaw

5. Non-Resident Nepali (NRN) Act and NRN Rules (2066)

NRN law and rules set out the rights of Non-Resident Nepalis to acquire, hold, and transfer property. NRNs of Nepali origin have special rights (subject to limits on agricultural land, ceilings, and procedural formalities). NRN cardholders must still follow registration and tax obligations.

6. Nepal Citizenship Act & Regulations

Citizenship laws define who is a Nepali citizen (and therefore eligible for unrestricted land ownership). Issues of dual citizenship and loss/gain of citizenship can affect property rights.

7. Local Municipal Bye-Laws & Zoning

Municipalities and local governments regulate land use, building permits, and occupancy — buyers must ensure the intended use (residential/commercial/industrial) complies with local zoning and building codes.

Who Exactly can Buy Rental Property in Nepal

1) Nepali citizens

Full ownership rights (subject to parcel-specific rules like ceilings in certain zones and other statutory restrictions). Register at the local Land Revenue Office (Malpot) and get Lalpurja/khatiyan for title evidence. See Lands Act and local Malpot procedures.

2) Non-Resident Nepalis (NRNs)

NRNs of Nepali origin can buy and own houses, apartments, and land (except some agricultural categories) within limits under NRN rules.

The NRN card and documentation simplify several processes, but practical rules still require registration, tax compliance, and sometimes MOFA attestation for document authentication. NRNs should follow the NRN Rules and consult the local Malpot.

3) Foreign Nationals (non-Nepalese)

General rule: Foreign individuals cannot acquire land in their personal name. Exceptions are narrow and require explicit government approvals. Common lawful routes for foreigners include:

- Leases: Long-term leases (commonly up to 30 years, renewable) for residential, commercial, and industrial use are widely used.

- Investment through a Nepal-registered company: A company registered in Nepal (with foreign investment approval under FITTA or DOI/IBN procedures) may acquire land necessary for its approved business operations. This is the standard route for foreign direct investment in land-intensive projects.

- Inheritance or prior ownership: Persons of Nepali origin who held property as Nepali citizens before losing citizenship or NRN card holders may have rights under specific transitional provisions (documented under Civil Code / NRN rules). Always verify via a lawyer.

Practical Legal Restrictions Commonly Encountered

- Agricultural land: Often restricted for sale to non-agricultural buyers (including NRNs and foreigners); many local rules cap the area a non-resident or an individual may hold. Check Lands Act and district rules.

- Ceilings & distribution: Historical land reforms instituted ceilings on ownership in some contexts (see Lands Act amendments).

- Repatriation of sale proceeds: FITTA and related rules regulate the repatriation of profits and capital for approved foreign investments. Private foreign nationals selling land may face foreign exchange controls and approval requirements.

Where to Buy Rental Property: Choosing the Right Location

Location determines demand, vacancy, and yields. Consider:

- Urban core (Kathmandu Lalitpur): Higher purchase prices, stable long-term demand from professionals and students; typical gross yields ~5–7%.

- Tourist hubs (Pokhara, Thamel in Kathmandu): Good for short-term rentals and AirBnB; potential for higher seasonal income but also higher management effort. STR (short-term rental) reports for Kathmandu indicate viable Airbnb markets in select neighborhoods.

- Secondary cities (Bhairahawa, Biratnagar, Chitwan): Lower entry price, rising rental demand as commerce and industry expand. Localized projects show strong rental activity in these growth centers.

Use listing portals, market reports, and local agents to compare rental rates and asking prices. Always compute expected gross and net yield for each micro-location before deciding.

Financing the Rental Property: How to Fund Your Purchase

Most buyers use some combination of personal equity and bank financing. Points to note:

- Mortgage availability: Nepali banks and DFIs offer housing loans. Mortgage credit interest rates averaged around 8–11% (varies by bank and borrower profile). Check Nepal Rastra Bank and individual bank offers for current terms.

- Loan-to-value (LTV): Banks typically finance a proportion of property value (commonly 60–80% depending on property type and borrower credit). Confirm with the lending bank.

- Documentation: Banks require title, Lalpurja/Khatiyan, valuation, and proof of income. NRNs/foreigners may face stricter terms.

- Alternatives: Joint purchase with family, developer financing, or seller installments are common in Nepal.

Always run cash-flow sensitivity: consider higher vacancy, maintenance, and interest rate changes when modeling returns.

Due Diligence Checklist to Buy Rental Property

Before signing any Agreement, complete these checks:

- Title & ownership documents: Obtain Lalpurja/khatiyan and verify with Malpot (Land Revenue Office). Use the HouseLand or local Malpot guides for document lists and steps.

- Land use & zoning: Confirm land is permitted for residential rental use and check any municipal restrictions.

- Encumbrances & taxes: Obtain an encumbrance certificate or ask Malpot for any mortgage or litigation claims.

- Construction approvals: Verify building permits and completion certificates from the municipality.

- Survey & area verification: Cross-check property area with the registered area.

- Check rental market & tenancy history: Ask for historical occupancy, rental rates, and tenant profiles.

- Physical inspection: Structural, MEP (electrical/plumbing), and drainage checks — hire a local civil/structural engineer if needed.

- Tax compliance: Verify the seller’s tax receipts and that property taxes are paid.

Due diligence reduces legal and financial surprises; therefore, don’t skip it.

The Step-by-Step Purchase Process

- Shortlist properties using portals, agents, and site visits.

- Negotiate price & terms (include earnest money or booking deposit).

- Sign a Sale-Purchase Agreement (SPA) with clear conditions—payment schedule, possession date, and contingencies.

- Obtain a valuation report for bank financing if using mortgage.

- Apply for bank loan (submit SPA, Lalpurja, tax receipts, KYC).

- Complete stamp duty & taxes: Pay registration fees, stamp duty, and applicable taxes. Typical buying costs are relatively low in Nepal compared to some countries but vary by municipality—check Malpot guidance.

- Register the transfer at Malpot: The buyer and seller must appear (or their agents with power of attorney) to record the transfer and issue new Lalpurja.

- Possession & handover: Collect keys, meter transfers, and any building warranties.

Always ensure payments are traceable (bank transfer) and retain receipts for tax and legal safety.

Taxation on Rental Income & Compliance

Rental income in Nepal is taxable. Current rules and practical slabs can change annually, so check the Inland Revenue Department (IRD) and tax advisory publications. Generally:

- Rental income is treated as income from house property and taxed at progressive rates; there are allowable deductions for maintenance and expenses. Recent tax guidance and PKF/Baker Tilly summaries outline rates and filing requirements for FY 2081-82 (2024–25).

- Withholding: Tenants (especially businesses) may be required to withhold taxes on rent; landlords must register and file returns. Local tax advisory articles summarize practical slabs and compliance thresholds.

Therefore, register with IRD, keep proper accounts, and consult a tax professional to optimize deductions and ensure compliance.

Managing the Rental Property (Operations & Tenancy)

After acquisition, day-to-day management determines profitability:

- Decide management model: self-manage, hire a property manager, or use a leasing agency. For tourists/short-term rentals choose professional managers for listings and turnovers.

- Draft strong tenancy agreements: Include rent, deposit, notice periods, maintenance responsibilities, and dispute resolution. Use standardized formats and register long-term leases with local authorities if required.

- Maintenance & capital expenditure: Budget typically 5–10% of gross rent annually for repairs, plus periodic rehabilitation.

- Tenant screening: Insist on IDs, references, and security deposits to reduce default risk.

- Rent collection & legal recourse: Use bank ECS/direct transfer where possible and be aware of landlord-tenant laws for eviction and dispute resolution.

Good operations lift net yields and reduce vacancy risk.

Calculating Returns & a Sample ROI Model

To evaluate, compute:

- Gross yield = (Annual rent / Purchase price) × 100

- Net yield = (Annual rent − annual costs (tax, maintenance, management fees, loan interest)) / Purchase price × 100

Example: Buy a Kathmandu apartment for NPR 2,500,000 and rent it for NPR 12,500/month (NPR 150,000/year).

- Gross yield = (150,000 / 2,500,000) × 100 = 6%.

- If annual costs (tax, maintenance, management, interest) = NPR 60,000 → Net income = 90,000; Net yield = 3.6%.

Always stress-test for 20–30% vacancy, interest rate rise, and higher repairs to see worst-case returns.

Risks and how to mitigate them

- Regulatory/ownership risk: Mitigate with full title search and lawyer review.

- Market risk: Diversify locations or property types; avoid over-leveraging.

- Tenant risk: Use strong lease terms and deposits; screen tenants.

- Liquidity risk: Property is illiquid plan exit timelines and hold periods.

- Operational risk: Hire competent property managers or maintain a reserve fund.

Prudent planning reduces downside significantly.

Conclusion

Buying rental property in Nepal can deliver steady passive income and long-term capital gains. Nevertheless, success depends on location choice, legal clarity, disciplined due diligence, realistic finance modeling, and professional management.

In short, be data-driven, seek local professional help (lawyer, valuer, tax advisor), and plan cash flows conservatively.

Read More: Real Estate Inflation Impact in Nepal: How Inflation Affects Property Prices